Starting personal finance can seem incredibly intimidating. From understanding credit scores to sorting through a plethora of budgeting apps and making sense of investing platforms—it’s simple to feel lost before you even start. That’s why we’ve distilled it all into an easy, beginner 5-step process to ensure you become genuinely financially literate and comfortable with your money in 2025.

Whether you’re a student juggling tuition and part-time jobs, a young professional beginning your career, or simply a person willing to take firm control of your financial future, this 5-step financial literacy roadmap will prepare you with the fundamental tools, real-world strategies, and confident mindset you need to succeed.

Learn more: Financial Literacy 101: How to Master Money Management

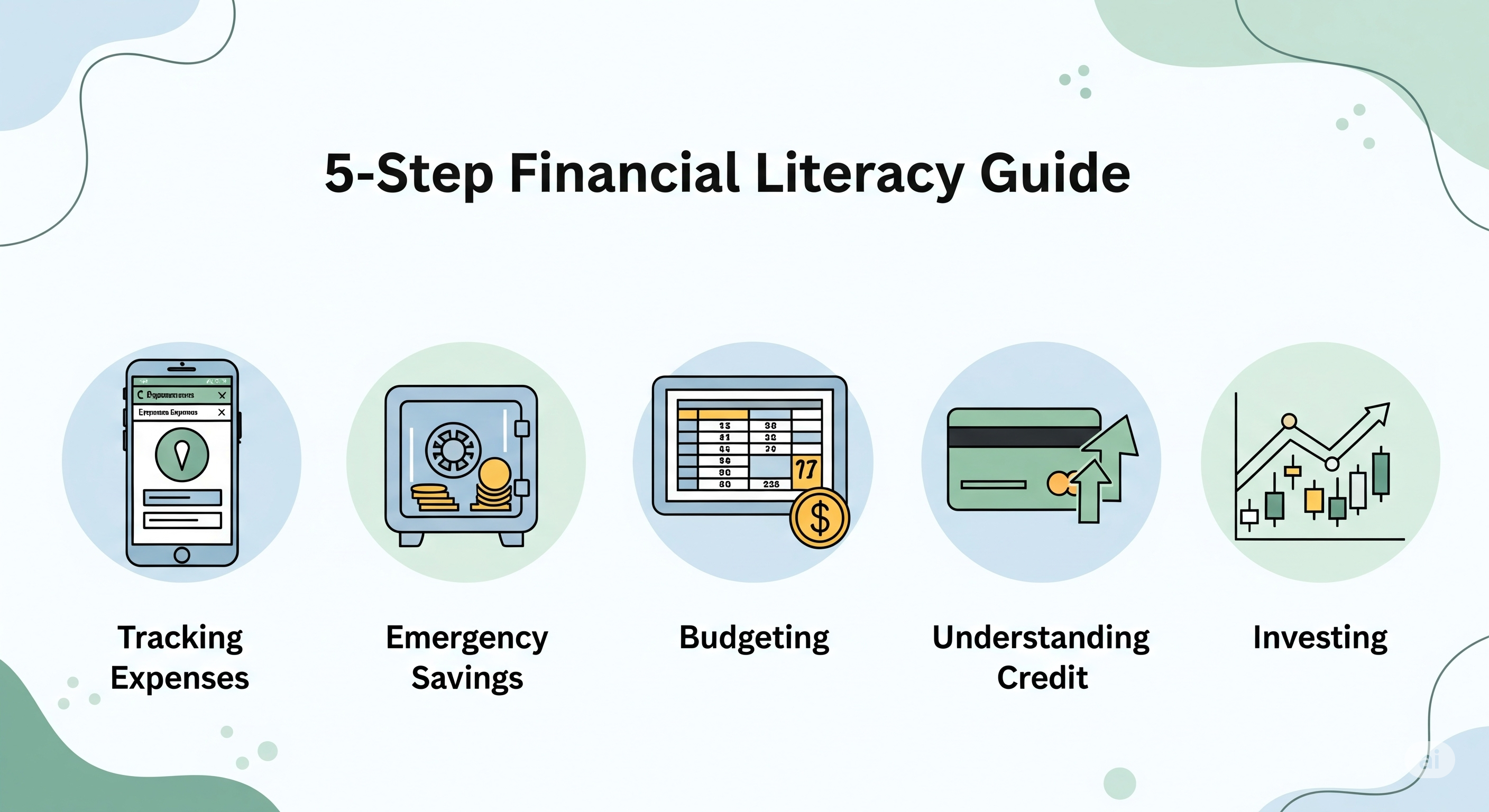

🧭 The 5-Step Beginner Framework for Financial Literacy

Small, steady steps create momentum and build confidence. Here is your guide to getting control of your money, one smart step at a time.

✅ Step 1: Track Your Spending

You can’t really manage or budget your money until you have a clear idea where it’s actually going. This first step is essential for developing an awareness of and understanding of your own spending patterns.

How To: With specific tools such as Mint, PocketGuard, or even a simple spreadsheet.

Action: Follow every single dollar you spend for a minimum of 30 days.

Why This Matters: Seeing where your money goes is the key to actually being in control of it. Most people are actually amazed to find their “spending leaks”—such as that morning coffee habit that really adds up!

Use our smart tool: 50/30/20 Budget Calculator – A Simple Rule for Smarter Money Management

✅ Step 2: Create a Realistic Budget

After you’ve diligently monitored your expenditure and determined patterns, you can create an intentional plan. A basic monthly budget gives a “job” to each dollar you make, which helps keep you from mindless spending and enables you to order your financial goals.

Establish Your Goals First: Identify what you’re saving for (e.g., an emergency fund, a down payment, credit card debt pay-off). Your budget should be a direct tool to meet these exact financial objectives.

Approaches: Apply popular budgeting methods such as:

50/30/20 Rule: Split 50% of your income to needs, 30% to wants, and 20% to savings/debt repayment.

Zero-based budgeting: Assign a purpose to every single dollar, so your income minus expenses is equal to zero.

Apps: YNAB, Goodbudget, or budgeting capabilities through your bank.

Try Free tool: Master Your Finances with a Monthly Budget Planner

✅ Step 3: Build Emergency Savings

A solid emergency fund is your financial safety net. It keeps you from having to borrow money when unexpected life situations—such as a car repair, medical expense, or job loss—inevitably strike.

Short-Term Goal: Target $500–$1,000 initially. This amount can fund numerous typical minor emergencies.

Long-Term Goal: Incrementally accumulate this fund to finance 3–6 months of basic living costs.

How To: Make it automatic by arranging regular transfers through your bank or through apps such as Chime. Make it easy!

Basic Protection: As a component of your financial safety net, also include basic insurance protection (e.g., health, auto, renter’s/homeowner’s) to shield yourself from greater, unexpected financial disasters.

Use our Emergency Fund Calculator – How Much Do You Need to Save?

✅ Step 4: Understand Credit and Debt

For financial literacy newbies, knowledge of credit and debt is essential. Your credit score has an effect on nearly everything—from qualifying for a loan or a credit card to finding an apartment or even affecting some career opportunities. Learn the fundamentals of how credit cards, various forms of loans, and credit reports really operate.

Key Concepts: Understand how your credit score is determined, why your debt-to-income level is important, and how interest rates affect you.

Debt Repayment: If you’re already in debt, prioritize developing a solid repayment strategy. The most popular strategies are:

Debt Snowball: Pay off your lowest balance debts first, achieving psychological momentum.

Debt Avalanche: Pay off high-interest debts first, which will cost you less money over time.

Tools: Monitor your credit health using Credit Karma or FICO Score Checker.

Pro Tip: Try to pay your credit card balance in full every month to not pay a lot of interest and to regularly improve your credit score.

Use our Free Credit Card Payoff Calculator – Get Debt-Free Smarter

✅ Step 5: Start Investing Early

You absolutely do not need to be rich to start investing. Even modest amounts invested consistently can grow significantly over time, thanks to the magic of compound interest.

Compound Interest Power: Starting early leverages the power of compound interest, allowing even small, regular investments to grow exponentially over time. Your future self will profoundly thank you!

How To Begin: Start with intuitive apps such as Acorns (for micro-investing), Robinhood (for trading, exercise caution), or a Roth IRA (for tax-favored retirement savings).

Beginner Tip: Low-cost index funds or ETFs can be an easy way to diversify your investments without requiring extensive market expertise.

Try Compound Interest Calculator : compound interest allows your money to grow on both the initial amount and the interest it has already earned

🔗 Helpful Resources & Tools to Support Your Journey

To help you put these steps into action, here are some highly recommended resources and tools:

- Budgeting: YNAB, Mint, Goodbudget

- Credit Monitoring: Credit Karma, Experian

- Saving & Investing: Chime, Robinhood, Stash

- Learning Platforms: Coursera, Skillshare, Khan Academy

Why This Matters

Surveys consistently show that a lack of personal finance knowledge can be costly. For example, studies indicate that the average individual can lose thousands each year due to avoidable financial mistakes or missed opportunities stemming from a lack of literacy. Don’t let confusion cost you. Start with this simple 5-step financial literacy guide and take control of your money—one smart step at a time.

Join our free newsletter and get weekly tips, practical tools, and money challenges directly to your inbox. It’s your direct line to accelerated financial growth!

One Comment